.jpg)

.jpg)

|

||||||||||||||||||||||||||

CLAL

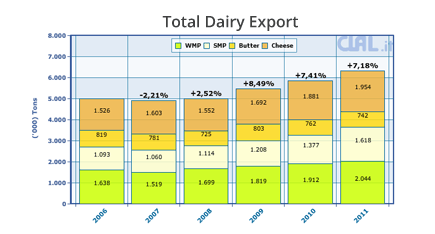

Dairy world trade

CLAL.it outlines the import and export trade flows of Cheese, Butter and AMF, Milk Powders, Whey and WPC, Condensed Milk, Packed and Bulk Milk, Lactose, Casein and Caseinates by the main international players.

enter

enter

Slideshow

CLAL.it provides with some training paths, updated in real-time and useful to market analysis during workshops and project works.

enter

enter

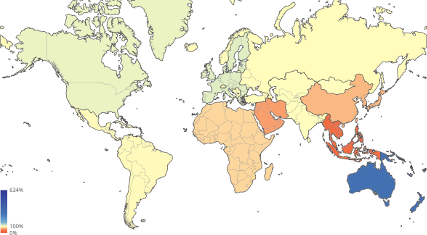

Milk Atlas

CLAL.it provides with a snapshot of the Milk production and livestock (cow, buffalo, goat, sheep, camel) and a number of interactive maps that visualize Milk Self-sufficiency worldwide.

enter

enter

subscribe

subscribe

CLAL News is an information service on the national and international dairy market, developed by the CLAL Team and Leo Bertozzi.

The information is addressed to all operators in the sector and concerns the market, product innovation, the strategies of the major companies and retailers.

On the right you can find the latest news in English language.

CLAL News is mobile-friendly: use the QR code to access from your smartphone